gilaxia/E+ via Getty Images

A Quick Take On Driven Brands

Driven Brands (DRVN) went public in January 2021, raising $700 million in gross proceeds in an IPO priced at $22.00 per share.

The firm provides a range of maintenance and repair services for automobiles in the United States.

As the Covid-19 pandemic wanes and inflation plateaus and then drops in the quarters ahead (my view), DRVN looks well-positioned to continue its growth trajectory.

My medium-term outlook on DRVN at around $29.00 is a Buy.

Company

Charlotte, North Carolina-based Driven Brands was founded to develop an asset-light business model of corporate-owned and franchised consumer and commercial automotive maintenance services.

Management is headed by president, CEO, and Director Jonathan Fitzpatrick, who has been with the firm since 2021 and was previously in various senior roles at Burger King Corporation.

The company’s primary offerings include:

The company advertises its various brand offerings through a combination of traditional, digital and offline advertising as well as through locating its stores in visible areas to significant drive-by traffic.

DRVN has a total base of 4,100 company-owned and franchised locations in the U.S. (49 states) and 14 other countries.

Driven’s Market & Competition

According to a 2020 market research report by First Research, the global automotive repair and maintenance services market is estimated to grow at a double-digit compound annual growth rate from 2015 to 2025.

A significant source of the forecasted growth will be from growing vehicle production in emerging markets such as India and China.

The U.S. auto repair industry is currently valued at around $115 billion in annual revenue and is highly fragmented, with an estimated 162,000 establishments, both single-location firms and companies with multiple locations.

It is estimated that the 50 largest repair and maintenance companies account for less than 10{7b5a5d0e414f5ae9befbbfe0565391237b22ed5a572478ce6579290fab1e7f91} of total revenue.

The company faces significant competition from a variety of sources:

DRVN’s Recent Financial Performance

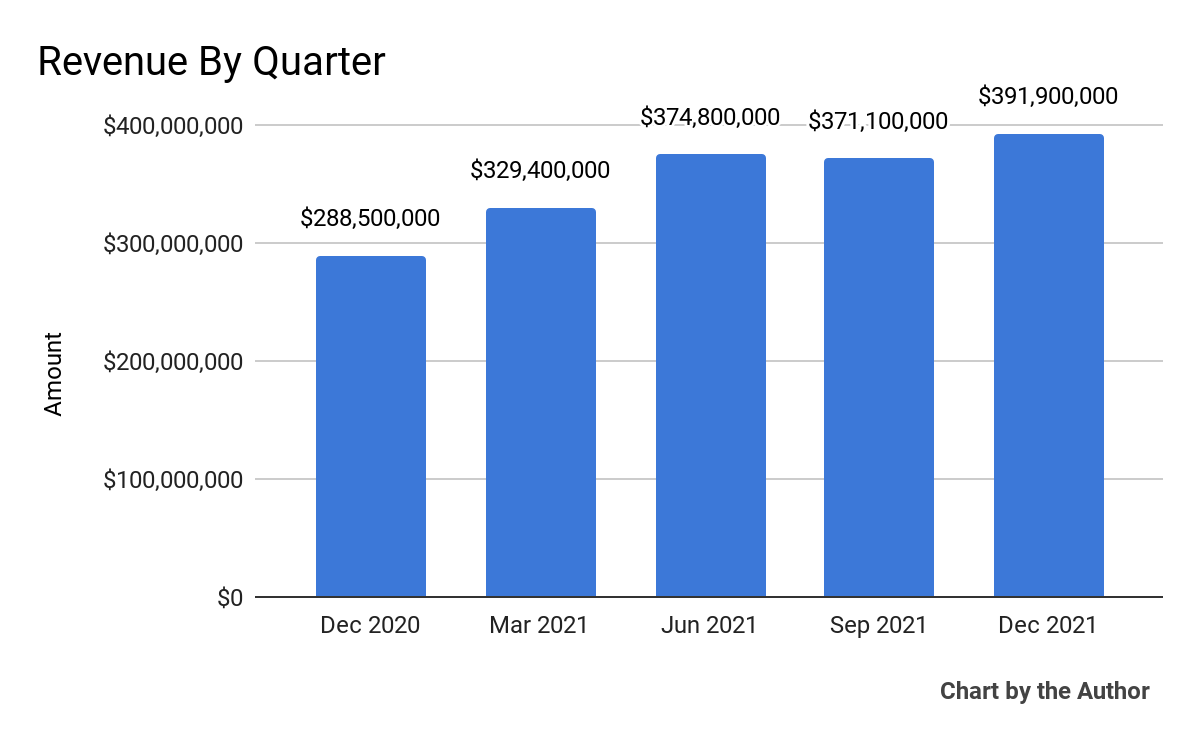

5-Quarter Total Revenue (Seeking Alpha and The Author)

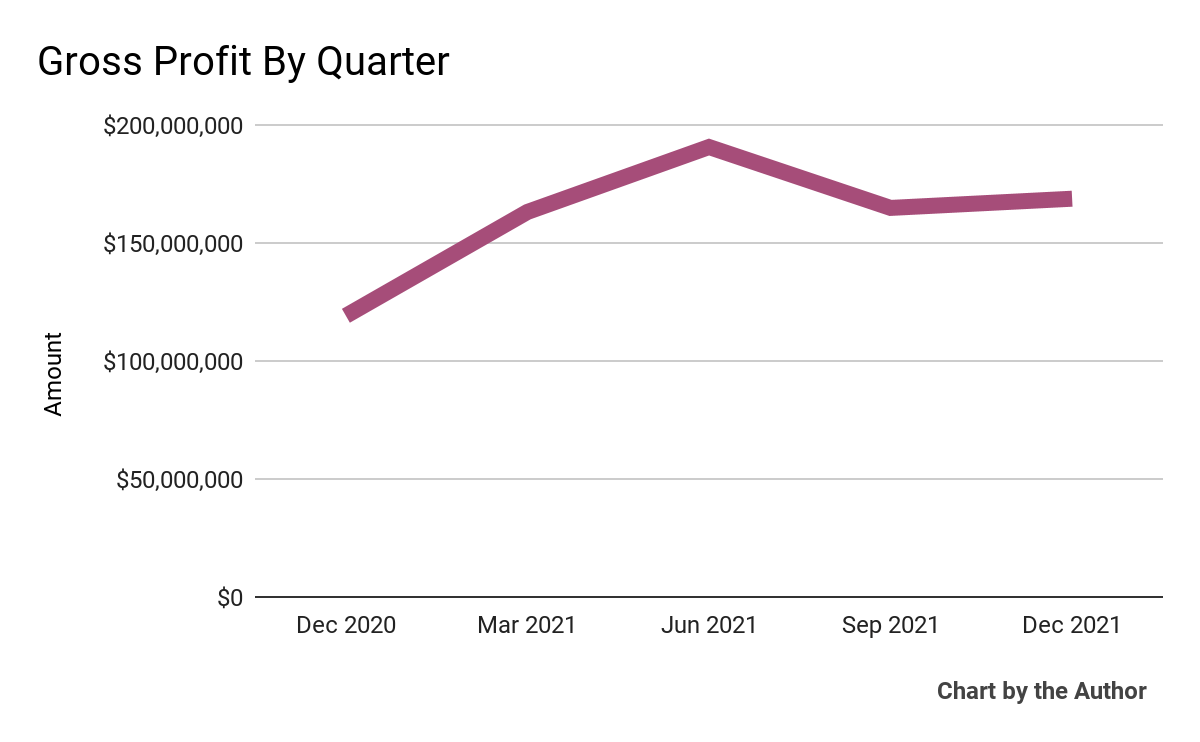

5-Quarter Gross Profit (Seeking Alpha and The Author)

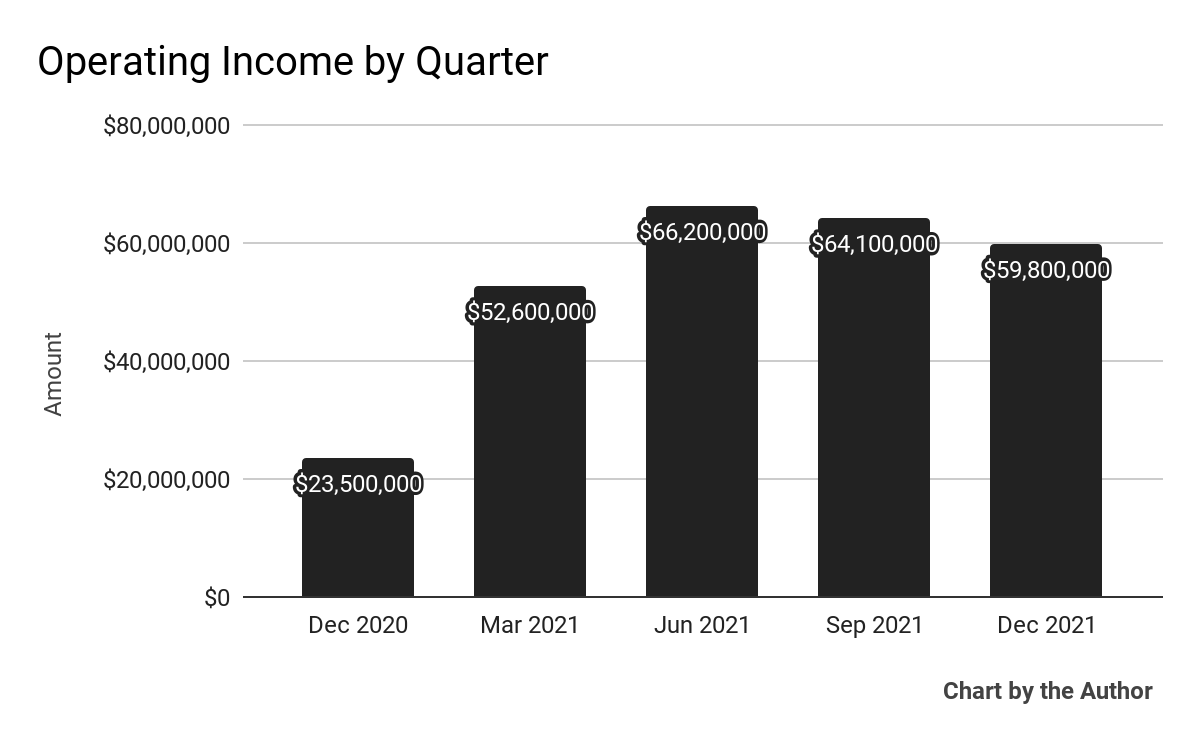

5-Quarter Operating Income (Seeking Alpha and The Author)

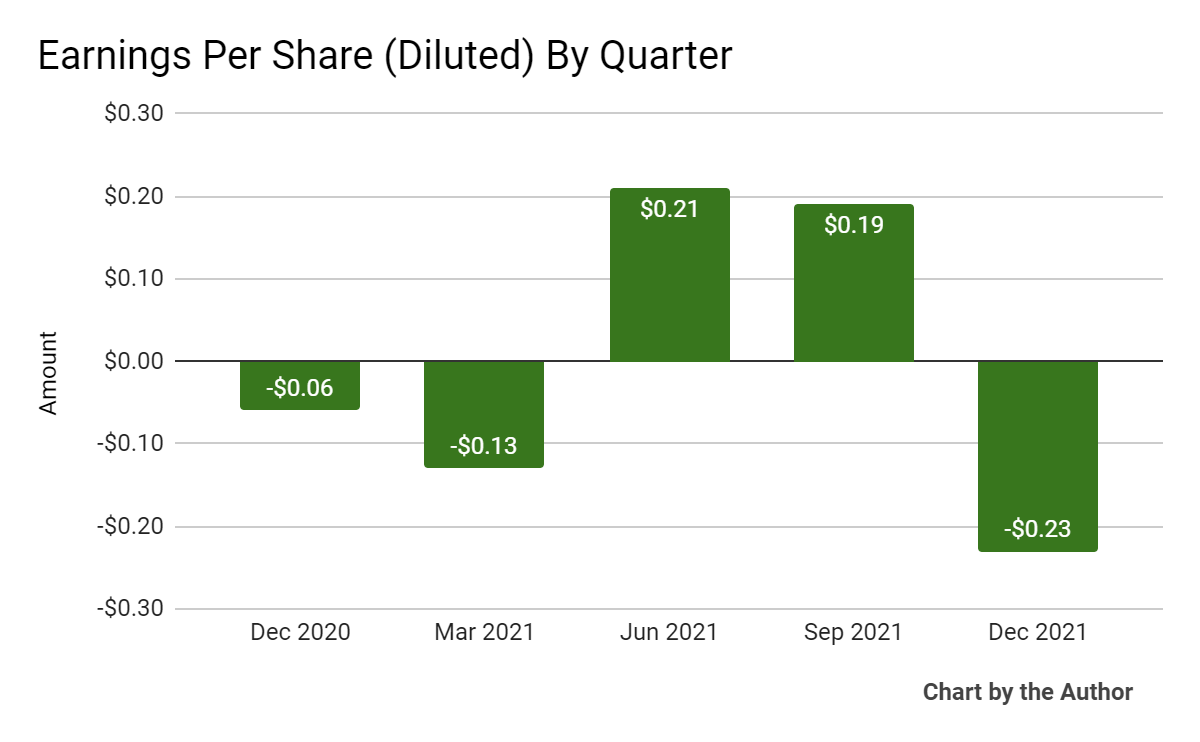

5-Quarter Earnings Per Share (Seeking Alpha and The Author)

(Source data for above GAAP financial charts)

In the past 12 months, DRVN’s stock price has dropped 6.1 percent vs. the U.S. S&P 500 index’s rise of 11.2 percent, as the chart below indicates:

52-Week Stock Price (Seeking Alpha)

(Source)

Valuation Metrics For DRVN

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure |

Amount |

|

Market Capitalization |

$4,830,000,000 |

|

Enterprise Value |

$7,620,000,000 |

|

Price/Sales |

3.16 |

|

Enterprise Value/Sales |

5.19 |

|

Enterprise Value / EBITDA |

21.43 |

|

Free Cash Flow [TTM] |

$218,910,000 |

|

Revenue Growth Rate [TTM] |

62.27{7b5a5d0e414f5ae9befbbfe0565391237b22ed5a572478ce6579290fab1e7f91} |

|

Earnings Per Share |

$0.04 |

(Source)

Commentary On Driven Brands

In its last earnings call, covering FQ4 2021’s results, management highlighted both its diversified revenue streams as well as its diversified go-to-market model where it can ‘build, but or franchise’ as desired.

Additionally, its asset-light business model produces strong cash flow and enables the company to reduce the impacts of inflation on its operations.

Also, its scale and public stock currency, when compared to many small local players, give DRVN an advantage.

As to its financial results, revenue grew by 36{7b5a5d0e414f5ae9befbbfe0565391237b22ed5a572478ce6579290fab1e7f91} and the firm added 247 net new stores in fiscal 2021.

However, management focused on adjusted EBITDA and EPS which are different and more optimistic than GAAP figures.

Looking ahead, management plans to focus its priorities on its Driven, Quick Lube, car wash and glass segments.

It likes these businesses due to their ‘simple operating models, highly fragmented competition, significant white space in terms of unit growth, and very strong unit level economics.’

The company’s M&A pipeline was described as ‘robust, and we are aggressively growing our footprint.’

The primary risk to the company’s outlook is a labor shortage, although management said it had ‘largely overcome the effects of the national labor shortage.’

Also, as the economy improves post-Covid, M&A opportunities may be fewer and more expensive, increasing its acquisition budget as target businesses perform better and seek higher valuation multiples.

A potential upside catalyst is that since the firm’s revenues come primarily from franchises, as the economy improves there may be more growth from this segment as would-be franchisees make their move to begin a first store or expand their existing store footprint.

In all, DRVN has performed very well during a difficult time period and is ahead of its pre-IPO projections.

As the Covid-19 pandemic wanes and inflation plateaus and then drops in the quarters ahead (my view), DRVN looks well positioned to continue its growth trajectory.

My medium-term outlook on DRVN at around $29.00 is a Buy.